What a Reserve Study Covers

A reserve study is not a simple list of broken items; it is a long-term financial roadmap for your community’s physical assets. While a standard inspection notes what is currently wrong, a reserve study predicts what will break in the future and how much it will cost to fix. This distinction is critical for HOA board members who need to balance immediate maintenance with long-term solvency.

The process follows a strict three-part sequence defined by the Community Associations Institute (CAI) and the Kresge Foundation. First, you conduct a physical inventory of all common area components, from roofing systems to paving stones. Second, you estimate the remaining useful life of each component. Finally, you calculate the funding required to replace these items before they fail.

This structured approach moves you away from reactive spending. Instead of scrambling for emergency funds when a roof leaks, you have a schedule that dictates when to replace it. By anchoring your budgeting in physical reality rather than guesswork, you protect property values and ensure that special assessments remain a rare exception rather than a recurring rule.

Step 1: Inventory Physical Components

Before you can plan for the future, you need to know exactly what you own. The first step in building a reliable HOA reserve fund is a complete physical inventory of all common area assets. This isn’t just about counting fences or lights; it’s about identifying every component the association is responsible for maintaining or replacing.

Think of this inventory as your property’s medical chart. You can’t prescribe the right treatment—or budget for the right costs—if you don’t know what’s ailing the building. According to the Community Associations Institute (CAI), a reserve study begins with a comprehensive list of standard area components. This list forms the backbone of your financial planning, ensuring no major expense slips through the cracks.

Identify and Categorize Assets

Start by walking the property with a notebook or tablet. Break down the inventory into logical categories such as roofing, paving, plumbing, electrical systems, and landscaping infrastructure. For each category, list every distinct element. If your HOA manages a pool, count the pumps, filters, heaters, and tiles separately. If you have a clubhouse, include the HVAC unit, kitchen appliances, and flooring.

Be thorough but organized. The goal is to create a master list that leaves nothing to assumption. This list should include:

- Major Systems: Roof, HVAC, plumbing, electrical, elevators.

- Exterior Elements: Pavement, fencing, lighting, paint, siding.

- Amenities: Pool equipment, playground structures, fitness center equipment.

- Landscaping: Irrigation systems, trees, hedges, and hardscaping.

Assess Age and Condition

Once you have the list, estimate the remaining useful life of each component. This doesn’t require an engineer’s report right away—just a realistic assessment based on manufacturer guidelines and visual inspection. Look for signs of wear, tear, or impending failure. A roof that is 15 years old with visible granule loss needs a different budget than one that is 5 years old and in good shape.

Document Everything

Keep this inventory updated. Components get replaced, new ones get installed, and conditions change. A living document ensures that your reserve fund calculations remain accurate. Without this foundational step, any financial projections you make will be based on guesswork, not data.

To help you get started, here are some practical tools for organizing your inventory:

As an Amazon Associate, we may earn from qualifying purchases.

By completing this inventory, you transform vague worries about future costs into a concrete, manageable plan. This list is your starting point for the next steps: estimating costs and building your reserve fund.

Estimate remaining useful life

You cannot forecast cash flow without knowing when each component will actually fail. The goal here is to assign a realistic timeline to every item in your reserve inventory. This step bridges the gap between a simple list of parts and an actionable financial plan.

Start by reviewing the current condition of each asset. Is the roof showing early signs of wear, or is it near the end of its cycle? Use the Community Associations Institute (CAI) and the Kresge Foundation guidelines to help calibrate these estimates. These resources provide standard lifespans for common HOA assets, giving you a baseline to adjust based on your specific community’s maintenance history.

Be conservative in your estimates. It is better to overestimate the remaining life slightly than to underestimate it. Overestimating means you might have a surplus in a given year, which is manageable. Underestimating leads to special assessments or deferred maintenance, which costs more in the long run. Think of this as building a buffer into your timeline, not a rigid expiration date.

Once you have a lifespan for each component, you can calculate the annual funding requirement. This number tells you exactly how much to collect from homeowners each year to cover future replacements. Accuracy here prevents the shock of unexpected large expenses.

To help you track these lifespans and calculations, consider using dedicated reserve management software. These tools automate the math and keep your data organized for annual reviews.

- Spreadsheet-based tracking

- Easy to customize

- No subscription fees

As an Amazon Associate, we may earn from qualifying purchases.

Keep your useful life estimates under review. Conditions change, and maintenance quality varies. Re-evaluating these timelines annually ensures your reserve fund remains accurate and sufficient.

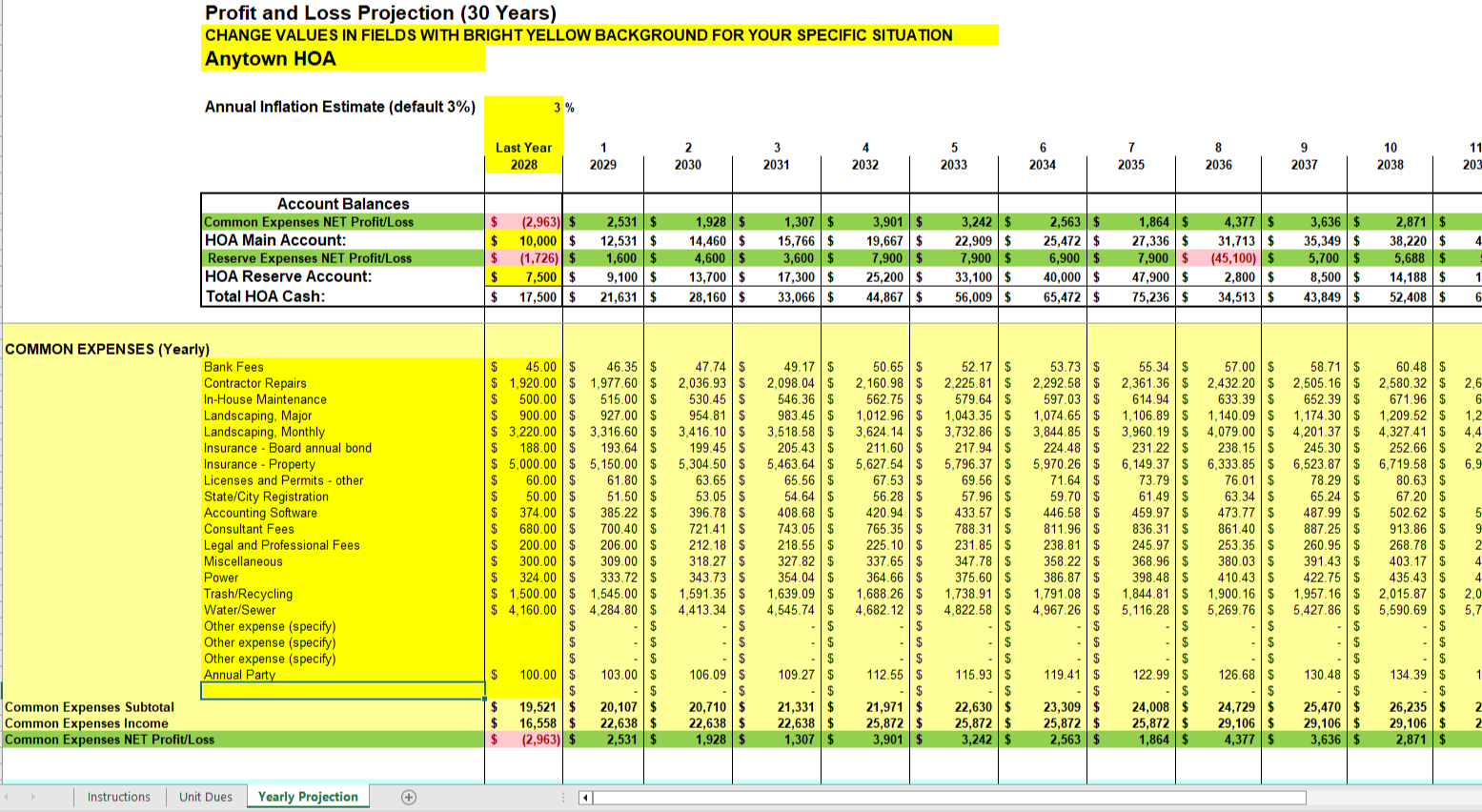

Calculate replacement costs

Now that you have inventoried your components and estimated their remaining useful life, it is time to put a price tag on the future. This step transforms abstract timelines into concrete financial targets. Without accurate cost estimates, your reserve fund is just a guess, not a plan.

Start by gathering current replacement costs for each component. Do not rely on quotes from ten years ago. Inflation and labor shortages have shifted the landscape significantly. Use the Component Replacement Cost Estimator from the Community Associations Institute (CAI) or the Kresge Foundation’s reserve study software to get localized, up-to-date pricing. These tools adjust for regional labor and material rates, giving you a baseline that reflects today’s market.

Next, project those costs forward to the year each component is expected to fail. A roof costing $50,000 today might cost $75,000 in fifteen years. A standard annual inflation rate of 3-5% is a safe starting point, but check local construction indices for more precision. This future value is the number that matters for your long-term funding plan.

Funding methods compared

Choosing how to collect these funds is as important as calculating them. The two most common approaches are Full Funding and Percent Funding. The table below compares how they impact your annual dues and reserve balance.

| Method | Target Balance | Annual Dues Stability | Risk Level |

|---|---|---|---|

| Full Funding | 100% of future costs | Higher initially, stable over time | Low |

| Percent Funding | 50-75% of future costs | Lower initially, volatile later | High |

Full funding aims to have enough money in the bank to cover every repair when it happens. This requires higher dues upfront but protects homeowners from special assessments later. Percent funding collects less each year, which keeps dues lower in the short term, but leaves a significant gap that must be closed later, often through risky special assessments or increased debt.

Tools for accurate estimation

Accurate estimation requires reliable data. While software does the heavy lifting, having the right reference materials on hand helps board members understand the scope of work. These resources provide the benchmarks needed to validate software outputs.

As an Amazon Associate, we may earn from qualifying purchases.

Common Mistakes in Reserve Planning

Even well-intentioned HOA boards stumble when managing reserve funds. The difference between a healthy reserve and a special assessment often comes down to avoiding three specific errors. By steering clear of these pitfalls, you can keep your community’s finances stable and predictable.

Underestimating Inflation

The most frequent mistake is using today’s prices for future repairs. A roof replacement that costs $50,000 today might cost $75,000 in ten years. If your reserve study ignores inflation, you will systematically underfund your account. Always apply a realistic inflation rate to your cost estimates to ensure you have enough cash when the project arrives.

Ignoring Minor Components

Boards often focus on big-ticket items like paving and roofing while neglecting smaller components. Light fixtures, painting, and pool equipment wear out faster than you might think. CAI-RMC notes that overlooking these minor expenses creates a false sense of security. A comprehensive inventory must include every asset, no matter how small, to prevent surprise shortfalls.

Skipping Regular Updates

A reserve study is not a one-time document. It should be updated every three to five years or whenever a major change occurs in the community. Conditions change, construction costs fluctuate, and maintenance practices improve. Sticking to an outdated plan means your funding schedule is likely wrong. Regular reviews keep your long-term financial health on track.

As an Amazon Associate, we may earn from qualifying purchases.

Essential Tools for Reserve Management

Accurate reserve records don’t happen by accident. They require a mix of structured data management and reliable reference materials. The California Association of Realtors (CAI) and the Kresge Foundation emphasize that successful reserve planning hinges on tracking component lifespans and costs with precision. To support this, boards need tools that simplify inventory, life estimation, and cost calculation.

Software and Tracking Systems

Modern reserve management software automates the tedious parts of the process. These platforms store component data, track depreciation schedules, and generate reports that align with CAI standards. Look for systems that allow easy updates to component conditions and costs, ensuring your reserve fund remains accurate over time.

Reference Guides and Templates

For boards managing reserves without dedicated software, comprehensive reserve study guides are invaluable. These resources provide templates for inventory lists, life expectancy tables, and cost estimation formulas. They help standardize your approach, making it easier to compare data across different components and years.

Practical Tools for Boards

The right tools can transform reserve management from a chore into a strategic advantage. Consider these essential items for your board toolkit:

- Comprehensive templates

- CAI standards alignment

- Step-by-step instructions

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!