What a Based Reserve Actually Constrains

When you look at a Based Reserve guide, the first thing to understand is that the reserve isn't a safety net for daily operations. It is a constraint on liquidity. The reserve acts as a buffer that must remain untouched to cover long-term liabilities, which means the capital sitting in it cannot be used for immediate growth or marketing spend. This distinction is critical because confusing reserve funds with operating cash is a common mistake that leads to insolvency.

In practice, this constraint manifests in four specific examples of reserves that organizations must account for:

- Dividend Equalization Reserves: These smooth out payout fluctuations, ensuring consistent returns even when profits dip in a given year.

- Debenture Redemption Reserves: Funds set aside specifically to pay back debt holders at maturity, removing the risk of default.

- Contingency Reserves: A flexible buffer for unexpected events, such as legal fees or sudden market shifts, that aren't covered by insurance.

- Capital Redemption Reserves: Capital gains that are locked in to maintain the company's capital base, often used to buy back shares without reducing equity.

Understanding these categories helps you see the Based Reserve not as a static number, but as a strategic tool. By knowing exactly which funds are locked and why, you can better plan your operational budget without accidentally dipping into capital that is legally or ethically bound to stay put. This clarity prevents the kind of liquidity crises that force companies to make desperate, short-term decisions.

Based reserve choices that change the plan

Choosing the right reserve structure involves balancing immediate liquidity against long-term stability. The four primary examples of reserves—Dividend Equalization, Debenture Redemption, Contingency, and Capital Redemption—serve distinct financial purposes. Selecting the wrong type can restrict cash flow or fail to protect against specific liabilities.

Dividend Equalization Reserves

This reserve smooths out dividend payments during volatile earnings periods. It allows a company to maintain a consistent payout ratio even when profits dip, signaling stability to shareholders. The tradeoff is that capital is locked away during lean years, reducing funds available for immediate reinvestment or expansion projects.

Debenture Redemption Reserves

Companies set aside funds specifically to repay debentures at maturity. This ensures that debt obligations are met without forcing a fire sale of assets or taking on new high-interest debt. While it protects creditor confidence, it reduces the free cash flow available for operational needs or new capital expenditures until the debt is retired.

Contingency Reserves

These act as a financial buffer for unexpected expenses, such as sudden regulatory fines or emergency repairs. They provide immediate liquidity when crises strike, preventing operational disruption. The downside is that excess contingency funds sitting idle represent an opportunity cost, as they are not generating returns or supporting growth initiatives.

Capital Redemption Reserves

Used to replace the capital value of shares bought back by a company, this reserve maintains the integrity of the balance sheet. It ensures that distributable profits are not used to erode the company's capital base. While it protects shareholder equity, it limits the amount of profit that can be distributed as dividends, potentially affecting short-term investor returns.

| Reserve Type | Primary Purpose | Liquidity Impact | Key Tradeoff |

|---|---|---|---|

| Dividend Equalization | Smooth payout consistency | Low during lean years | Restricts reinvestment funds |

| Debenture Redemption | Ensure debt repayment | Reduced free cash flow | Limits operational flexibility |

| Contingency | Cover unexpected expenses | High emergency access | Idle capital opportunity cost |

| Capital Redemption | Replace bought-back shares | Restricted dividend distribution | Lower short-term returns |

Turn research into a practical decision framework

A based reserve study provides the data; your governance team provides the strategy. Without a clear framework, accurate component analysis and funding models remain theoretical. This section outlines the operational steps to convert reserve data into enforceable financial policy.

Select the funding plan that matches the community’s financial reality. The choice typically falls between full funding (paying for components as they age) or partial funding (paying a lower baseline). This decision sets the trajectory for all future assessment increases and should be documented in the bylaws or a separate reserve policy.

Set clear limits on annual assessment increases to protect homeowners from sudden financial shocks. Define whether caps apply to the base assessment or the total fee, including supplemental charges for major repairs. Transparent escalation rules prevent legal disputes and ensure the reserve fund grows steadily even during periods of inflation.

Move reserve contributions from a line item to a fixed operational requirement. The board should treat the based reserve contribution as non-negotiable, adjusting it annually based on the study’s findings. This integration ensures that deferred maintenance does not accumulate, keeping the community’s assets in a state of good repair.

Provide homeowners with clear, annual updates on reserve fund performance. Use simple charts to show the gap between funded and actual reserves, and explain the impact of upcoming major projects. Regular communication builds trust and increases compliance with assessment payments, which is critical for maintaining long-term financial health.

As an Amazon Associate, we may earn from qualifying purchases.

Watch Out for Weak Reserve Options

When leveraging infrastructure tools for market research, it is easy to mistake a basic inventory for a strategic reserve. Many providers offer "basic" or "standard" studies that skip critical components. These weak options often lack the depth needed for accurate long-term financial planning.

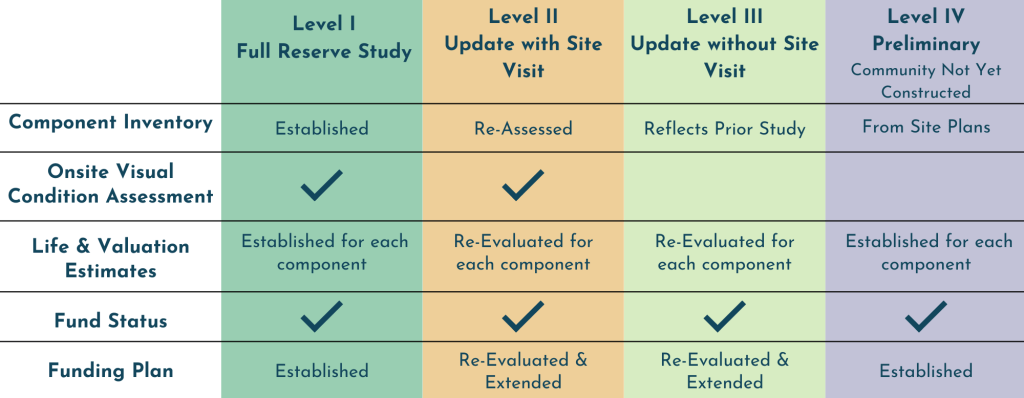

A common mistake is accepting a level 1 study when a level 2 is required. Level 1 studies rely on estimates and historical data without physical inspection. This approach can lead to significant underfunding if hidden deterioration exists. Always verify whether the study includes a full component inspection and remaining life analysis.

Another misleading claim is the promise of "guaranteed" accuracy without ongoing updates. Reserves are dynamic. A study that does not account for inflation, changing labor costs, or new regulatory requirements becomes obsolete quickly. Look for tools that offer regular re-evaluation and sensitivity analysis.

Be wary of options that bundle unrelated services without clear pricing. Some firms offer free reserve studies as a loss leader to sell more expensive consulting packages. This can create a conflict of interest. Ensure the core reserve study is transparently priced and independent of other service commitments.

Based reserve: what to check next

Before committing capital to reserve infrastructure, it helps to separate accounting definitions from practical application. The term "reserve" shifts meaning depending on whether you are looking at corporate balance sheets or physical asset management. Below are the most common questions regarding reserve structures and their strategic use.

No comments yet. Be the first to share your thoughts!